Spring/summer sports are in full swing. But the weather has been playing spoilsport. A lot. We’ve had about 4 days of outdoor activities cancelled due to rain. Things are looking good for this weekend forward though.

Till next month. Hope you all are enjoying spring, wherever you are. Cheers!

We went on an international trip straddling March and April. Travel, flights (9 in total, plus a helicopter ride!), time zone changes, pre-travel stress, post-travel jet lag ….all have contributed to our lives turned haywire for a number of weeks.

Spring has been quite wet here. Another 2 inches of rain in forecast over this weekend.

Hope you’re staying nice and warm, wherever you are. Cheers!

After one of the mildest winter on record – probably the warmest, by the time it ends – at the end of March we are in the midst of a 2-prong snow storm. Schools are likely to be cancelled for tomorrow and kids are rejoicing!

Lots going on for us. Spring activities season is starting up. We are going on an international trip for spring break.

March has shaped up nicely, in terms of the market gains.

Hope you’re having a good start to spring, wherever you are. Cheers!

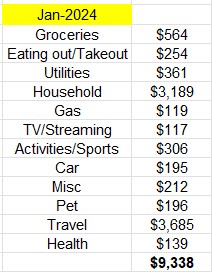

Spending was probably at an all time monthly high. We got a lot of stuff for the house and bought round trip airfares for an upcoming international trip.

Spring has made an early entry here. We’ve had 50°F days in January! That’s unheard of. A 70°F day is apparently in the forecast next week 😲

We are settling in at the new place. Hope you all are having mild winter wherever you are. Cheers!

We ended last year with our highest NW and the greatest increase, ~$300k, in NW in one year. Nice!

Since we started tracking and documenting our journey towards FIRE from beginning of 2017, we’re amazed how far we’ve come. In January 2017, our net worth stood at $458k. In 7 full years, we are over $1.6m. Incredible!

We made the following contributions to our investment accounts last year:

401(k) – $19,221 (only for W) – $440 less than in 2022

IRAs – $13k (combined for both) – hit goal of max limit; as we did in 2022

Brokerage – $2,700 – waaay below the $14.4k from 2022

529 – $2,200 – $200 more from 2022

HSA – $6,750 – $1k paid by employer, so we put in the max allowed

In all, we contributed $43,871 to our investments in 2023.

We took an international trip in 2023 – a 10 day long, utterly fabulous journey through one of the Scandinavian countries, bang in the middle of their glorious summer.

That trip, obviously, burned through cash. As did the little thing we did at the end of the year – bought a home! We have spent over $10k since we moved and a slew of known expenses lined up this year. That is the reason we are hoarding cash, more than we usually do. Liquid reserves of $102k at the end of the year has about $25k earmarked for travel (an international trip) and projects around the house, all before we hit the middle of the year. All this on top of a monthly mortgage payment that doubled from $1,200 to $2,400! But no complaints – we went into this knowing very well what the numbers were going to look like. We had been looking to move for almost 4 years and had given ourselves the end of 2023 to make it happen.

Goal for 2024:

IRA: Hit max limit of $7k individually; $14k for both

HSA: Hit max limit of $8,300 for families. W’s employer chips in with $1k, so out of pocket for us would be $7.3k

401(k): Hit $15k. It is likely we will go beyond this.

529: Minimum of $2,400. $3k would be a stretch goal.

……anything else would be just gravy

After our international trip in spring, we’re not sure how much we’ll travel this year. Maybe one more vacation during summer. A couple of road trips here and there. Setting up the new home will be the forefront this year.

We had some whopping numbers for the last month of last year.

In isolation, the $94k increase in FI funds is massive. But with the value of our new place being $280k more than our old place, drove NW up by $158k since November! Our NW stands at $1.66 million. Absolutely bonkers.

Winter, after being largely absent in 2023, has struck us with a fury in the new year. We’ve had multiple days of lows in negative single digits, with windchill reaching -20 to -30!!

No apologies, none whatsoever for publishing last month’s report ….two days before the current one ends 😀

We have valid reasons to not have any time. Make that a solitary valid reason.

We bought a house and moved!

And our lives, as far as we can recollect now, have been packing up, boxes, moving, unpacking, and settling down. Did I mention boxes? Yeah, right. More on that later …

Our NW increased by a whopping ~$98k last month! That’s, incredible – bordering the incredulous!

This month hasn’t been bad either.

Spending in November

Regular expenses were lower than average (~$4k) in November, only inflated by the $2k we spent on washer and dryer. This is primarily because we were setting up for the move in December and the bleeding we knew was waiting for us. We have spent over $10k this (December) month already – between hiring movers, getting rid of junk, and setting up the new place.

We will publish our yearly Incomes post in a day or two. Then the December NW post, followed by the end of the year review. The biggest question is, WHEN? Frankly, I don’t know. Hopefully, soon!

Here’s to a great year coming up for all – cheers!

Third consecutive month of decline. This time by $24k or 1.7% from September.

But this too shall pass. Things will get better 🙂

With this late of a post, we’re closer to Thanksgiving than Halloween! Not much update other than it has been a terribly mild fall so far. Activities are slower – November and December are typically our down months. I use “down” as relative to other months – we’re still out 2 nights a week.

Hope you all find something to be thankful for! We sure do – life has been good to us.

Net worth decreased in the second successive month, this time by over $52k or 3.5% from August.

Markets are doing what they do, and we’re riding the trough. All is good.

Expenses for September is right lower than the average of about $3.5k but that’s because we didn’t eat out or socialize as much. All due to sports ruling our lives in the month of September. We were lucky to have one evening where all 3 of us had dinner together. But it’s all our choice. We choose to be so inclined.

Fall is rather slowly descending where we are. After a severely drought ridden summer, rains have poured down in September and that has made plant life is very confused. They were ready to change color and shed their leaves early but the unseasonable rains have made them change their minds. Now, Oct 19, when typically would be past peak falls colors, this year we’re about 80% there.

Here’s a mild winter ahead (wishful thinking!). Cheers!