NW was down ~$10k for February. Which for March will turn a deep shade of red.

We are reaping some glorious spring weather, interspersed with school closures for snow! Another storm system is supposed to fly by tonight – kids are looking at the prospect of another day off tomorrow.

Hope you’re doing well, from wherever you’re reading this. Cheers!

We had an increase of $264k last year and ended with $1.9m in Net Worth.

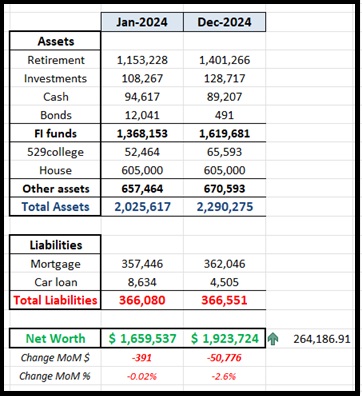

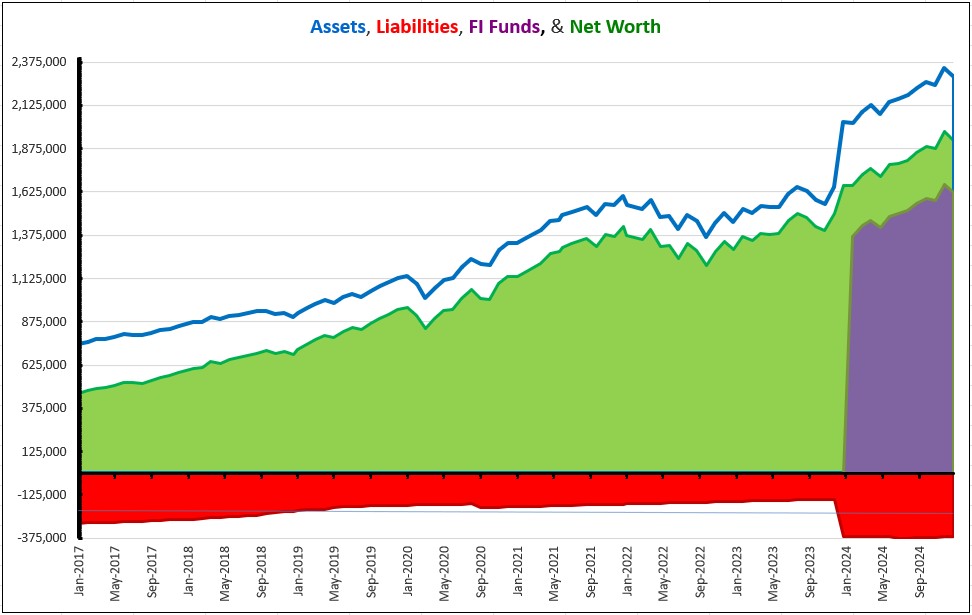

Since we started tracking and documenting our journey towards FIRE from beginning of 2017, we’re amazed how far we’ve come. In January 2017, our net worth stood at $458k. In 8 full years, we are over $1.9m. Whoa!

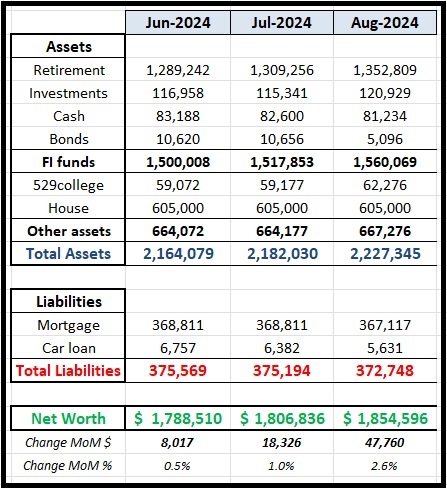

This year we added in the “FI Funds” in the visual. That is the value of our liquid investments.

We made the following contributions to our investment accounts last year:

401(k) – $14,954 (only for W) – $4,267 less than in 2023 but hit goal set last year

IRAs – $14k (combined for both) – hit goal of max limit; as we did in 2023

Brokerage – $0 – was $2,00 in 2023, and this wasn’t a priority last year

529 – $3,000 – $800 more than 2023, and hit stretch goal

HSA – $8,300 – $1k paid by employer, so we put in the max $7.3k allowed

In all, we contributed $39,254 to our investments in 2024.

We took a planned international trip last year, for us to see family. Then M had to make that same trip again, alone, as a parent passed away. Then another planned international trip for all three of us to one of the most expensive countries in Europe, over Thanksgiving. And then ….M took another trip back to take care of some things! A LOT of travel, and money spent on travel, this past year.

For 2025 we don’t have a single international trip planned. We do, however, anticipate quite a bit of road travel in domestically this year. We’ll see how that pans out.

Goal for 2025:

IRA: Hit max limit of $7k individually; $14k for both

HSA: Hit max limit of $8,550 for families. W’s employer chips in with $1k, so out of pocket for us would be $7,550

401(k): Hit $15k.

529: Minimum of $3,000. $3.5k would be a stretch goal.

Missed October’s post but this post will include those numbers.

After a minor blip in October, November had a massive upside. $95k addition to our net worth, which is a 5% increase from the last month. Biggest gain this year.

We had (another) international trip in November. For those who are counting, this was our third such trip this year! This trip was planned in summer to take advantage of discounted international flights during the Thanksgiving period. Round trip tickets to an expensive part of Europe were about $550 apiece. We met up with family – who live there and who visited from another part of the world to be there with us.

————————————————–

Spending for November

The expenses for the vacation in November was a tad over $2k and this included food, gas, entry tickets, tolls, merchandise, and incidentals. Flights, car, and lodging were already paid for earlier.

————————————————

And yes – the US elections happened. We are all very sad.

But here is to looking ahead and hoping for the best.

At this juncture – exactly two weeks before Americans go to the polls to elect the 47th President of the country – we would be amiss to mention what is at stake.

A convicted felon vs a prosecutor.

An adjudicated rapist vs a normal human being.

A con man who only works to enrich himself vs someone who has devoted her life to public service.

An openly racist and xenophobic individual vs someone who isn’t either.

A hateful, pitiful, angry man vs a big hearted, joyous woman.

An almost senile, almost octogenarian vs a sharp sexagenarian.

A misogynist who is on a spree to end access to women’s healthcare vs an advocate of women’s health.

A man who claims to be devoutly religious while peddling $60 bibles. A man who has cheated on each of his three wives; the current one with a pornstar when their child was a 3 months old.

A traitor who holds other dictators in high regard vs a senator and vice-president who works for the country.

Since we started this blog in February of 2017, last month – July 2024 – was the first time we did not publish a monthly update. 89 consecutive months of posting came to a crashing end.

One of our parents passed away in late July. A variety of health issues, combined with old age, had made the writing on the wall fairly clear. But nothing really prepares you for the 4 am phone call. Then leaving the country 7 hours later. Thirty-two hours of travel.

Anyway ….

We’re back into our school reopening mode now. I love September. The promise of new beginnings. Cool down. Fall sports. We actually went for our first kayak ride of the year yesterday.

Financially, ATH are everywhere. Markets are doing good.

The numbers would have been even higher if we hadn’t refinanced our mortgage. Let me explain.

When we bought our home last year, the best rate we got was 7.25%. Talks of multiple rate cuts by the Feds had us thinking that we’d refinance anyway in the not too distant future. In May, all murmur of rate cuts had died down. We shopped around for refinance rates. Got offered 5.875% by paying a bunch of points, with a lower monthly payment. But the math worked out – that is, we end up paying a lot less in overall interest, if we made the same monthly payment with the 7.25% rate.

So with closing costs and points baked into the new mortgage, the loan stood at $370k, up from the $355k at end of May.

We also paid the last tranche of payments to contractors for work around the house. This concludes all the big work that we had planned and budgeted for this year. Some of it was mandated by city code, some we wanted done. Since we moved, we have spent around $28k on material and labor, and countless other hours of sweat and wait.

Life in our neck of the woods has been pretty good. Mostly a mild summer, with lots of rain. We decided to not do extended summer travels as we’re going on (another) international trip later this year.

Hope you all are doing well, wherever you’re reading this from. Cheers!

Growth of 3.9% MoM, matching the increase in February.

Spending in May

Major category was Household, where we “splashed” out $2k on a new dining set that we’d ordered, but it was back-ordered, 6 months ago! We also purchased some art from a local art fair – encouraging local artists and filling up blank walls at our new place.

June’s numbers will be …different. We have completed a couple of major projects around the house – already budgeted for. We also refinanced our mortgage. Details coming.

It has been a summer of …rain. After droughts in the past couple of years, this year precipitation has more than made up for it. Numerous outdoor activities have been cancelled due to standing water and thunderstorms. Hoping for more familiar last 2 months of summer.