Earlier this month, Vanguard published this report on FIRE and set some anti-FIRE cats amongst the proverbial pigeons. You know, pigeons like us who have bought into the “idealogy” that you really can’t afford to be chained to a job for a paycheck for decades and decades. You need to get out of the rat race as soon as you can, as if your life depended on it.

The article, bullet-wise (as all good articles should have), talks about:

- the dangers of blindly following the 4% withdrawal rate (given how the market is expected to perform poorly over the next decade),

- using appropriate retirement horizons,

- the effect of the cost to invest,

- the importance of having a diversified portfolio, and lastly,

- the need to have a dynamic spending strategy

All true. And most rational people pursuing/in FIRE would say so. These factors are nothing new. The 4% SWR is not gospel, the recent returns of stocks is the outlier than the norm, investing costs are to be merciless slashes, diversifying, and having a spending strategy – and even an earning strategy in FIRE – that is flexible, are all built into the plan!

Here is the real, inflation adjusted, historical return YoY (CAGR) of the stock market since 1871. Yes, over 150 years worth of data. It stands at 7.06%, adjusting for inflation and reinvesting dividends, for over a century and half. You can select the time period you want – MoneyChimp Market CAGR.

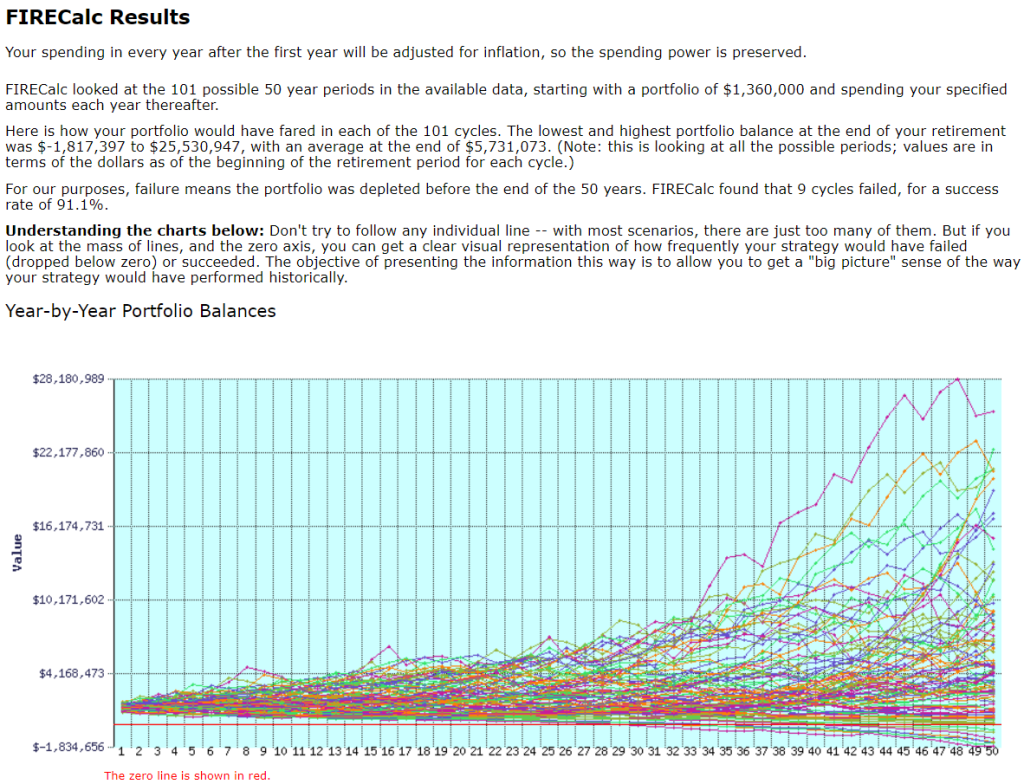

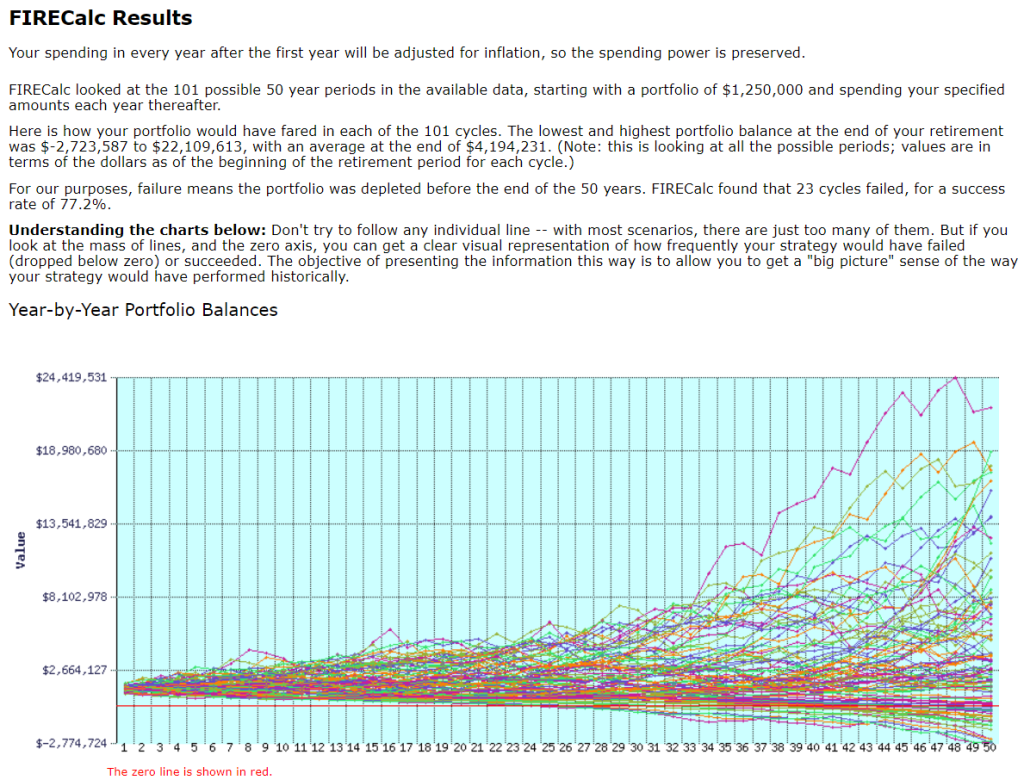

Here are two simulator applications, that runs multiple iterations (hundreds) of how a portfolio performs over extended draw down periods. I’ve run 3 simulations on each. (there are some underlying assumptions, such as stock/bonds allocation, expected inflation, etc. I encourage you to explore and play with the tools):

- Portfolio of $1.5M, expected spending of $50k/year, inflation adjusted, to last for 50 years, withdrawal rate of 3.33%

- Portfolio of $1.36M, expected spending of $50k/year, inflation adjusted, to last for 50 years, withdrawal rate of 3.67%

- Portfolio of $1.25M, expected spending of $50k/year, inflation adjusted, to last for 50 years, withdrawal rate of 4%

Scenario 1 – Success rate of 99%

Scenario 2 – Success rate of 93%

Scenario 3 – Success rate of 84%

firecalc (running the same 3 scenarios)

Scenario 1 – Success rate of 96%

Scenario 2 – Success rate of 91%

Scenario 3 – Success rate of 77%

If someone told me that I’d have between 77% and 84% success rate of an endeavor that I was about to embark on, I’d take those risks. But we are almost hard wired to be extra cautious about money. Especially our own money. So I understand if the 4% rule is bent into the 3.33% rule to get into the the 90% certainty range.

And, Vanguard keep those costs low. We’re all good here.