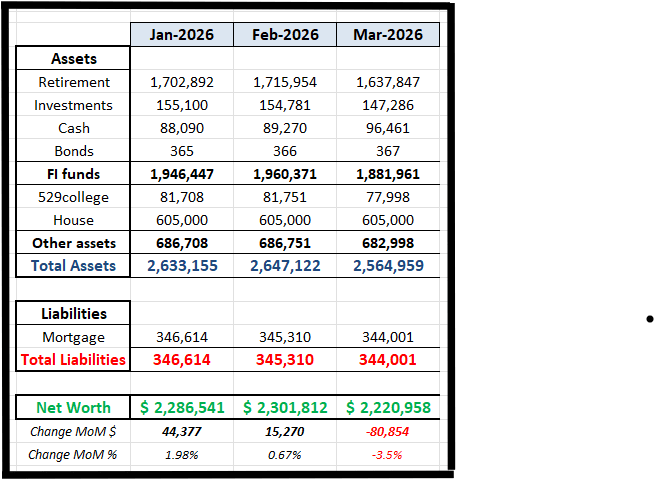

The first update for the year. January and February provided modest increase but in March the bottom sorta fell off. $80k in the red about 3.5% decrease from the previous month.

But it is fine 🙂

Spring sports season is officially underway. Between playing and coaching a combined total of 3 sports, we have little time for much else. We love the seasons where we are outside and active!

Here’s hoping you are having a great start to the year.

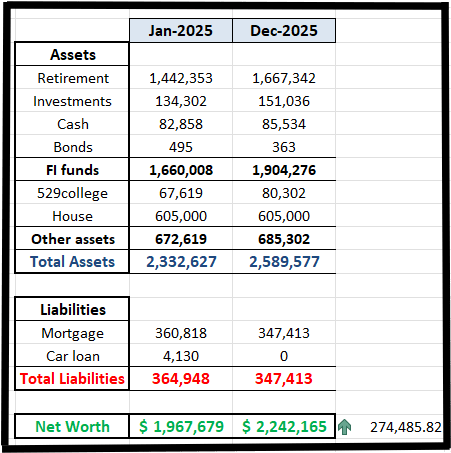

Net worth increased by $274k last year and ended the year at $2.2m.

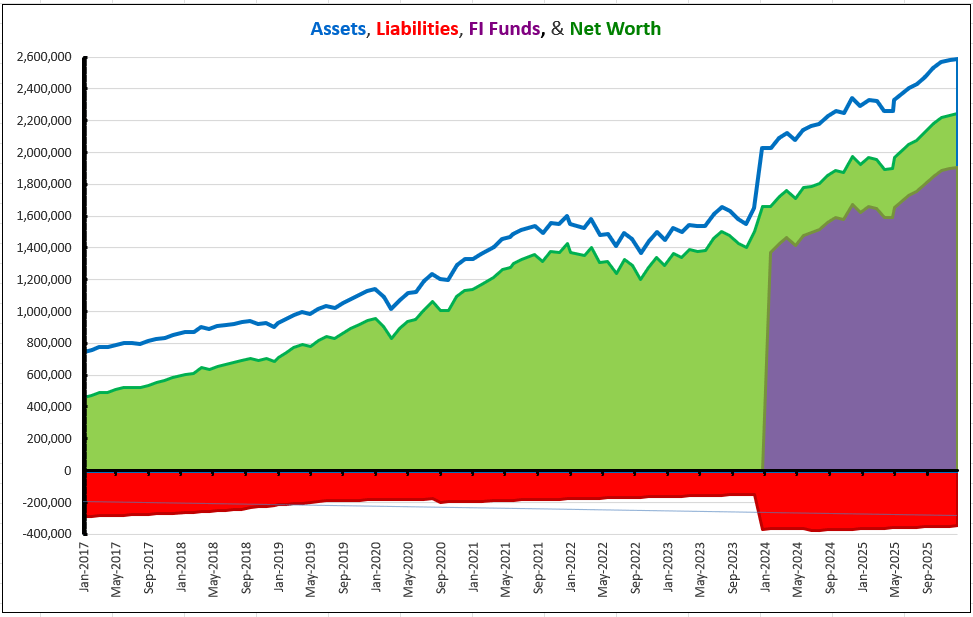

Since we started tracking and documenting our journey towards FIRE from beginning of 2017, we’re amazed how far we’ve come. In January 2017, our net worth stood at $458k. In 9 full years, we are over $2.2m. That is bonkers.

–

We made the following contributions to our investment accounts last year:

401(k) – $17,070 (only for W) – $2,116 more than in 2024 and went over the $15k goal set last year

IRAs – $14k (combined for both) – hit goal of max limit; as we did in 2024

Brokerage – $1,900 – was $0 in 2024, and wasn’t a goal for last year

529 – $3,400 – $400 more than 2024, and almost hit stretch goal of $3.5k

HSA – $8,550 – $1,200 paid by employer, so we put in the max $7,350 allowed

In all, we contributed $43,720 to our investments in 2025.

Goal for 2026:

IRA: Hit max limit of $7.5k individually; $15k for both

HSA: Hit max limit of $8,750 for families. W’s employer chips in with $1.2k, so out of pocket for us would be $7,550

At $3.8k, spending was on the higher side. Chalk some of it down to spending on gifts – for us and extended family. One of the larger purchase was whole new bed set for our child.

As the end of the year draws close, we have a few posts coming up in the beginning of the year.

Hope you are having a good holiday season, wherever you are. It’s on the colder side where we are. Our low for tonight is about 12 below 0 (Fahrenheit).

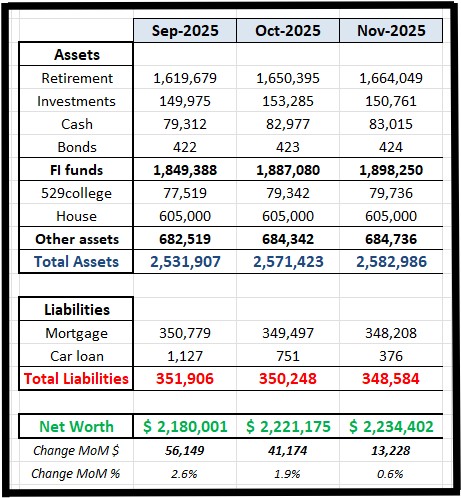

Another month of ATH, though the pace of increase has slowed down.

I suppose, the next milestone is to see the FI funds cross $2M.

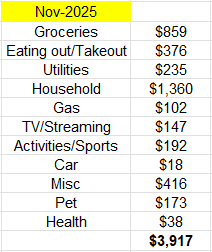

October has been a welcome change of pace from the chaos of early fall. Fall sports typically wrap up by early October and then we take it easy for the rest of the month. Winter training picks back up in November.

We are all doing well and thankful for everything we have going on in our lives. Hope all you readers have something to be thankful for.

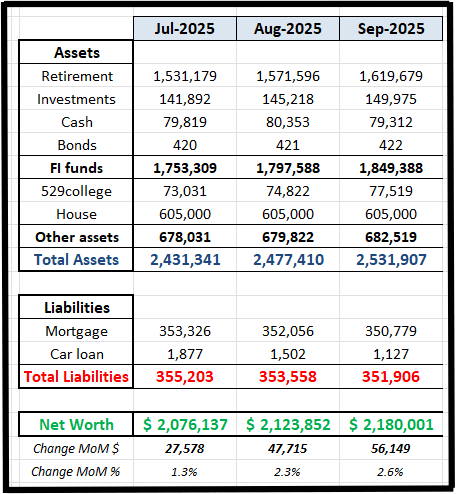

We breached the $2.5m mark in total assets. NW is at $2.18m and FI funds almost at $1.85m. All high water marks.

We missed to publish updates for July and August – I’ll put it down to the madness that engulfs our lives in late summer/early fall – start of the sports season. Especially HS sports.

Here is spending for September.

Hope you all are having a good start to fall. Cheers!

End of July signifies wrapping up spring/summer sports. And then turning around getting ready for “fall sports” to fire up the new season in mid August! When it comes to sports, we don’t play around 😀

It’s been an unusually hot end for July. With temps hovering around 100°F, we are glad to spend more time within the confines of artificial air conditioning.

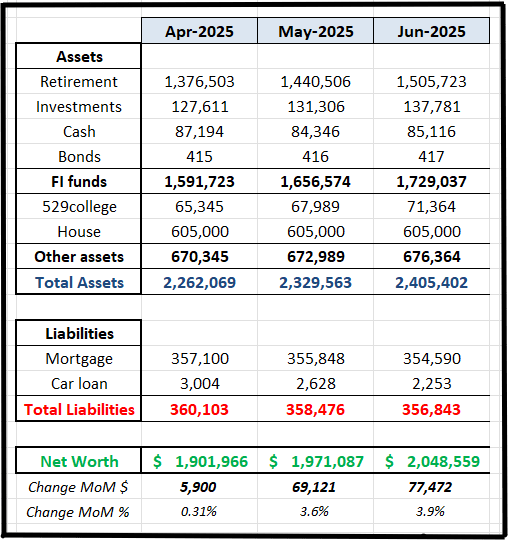

We saw a $69k increase in NW last month, a growth of 3.6% from the month before.

Spending in May

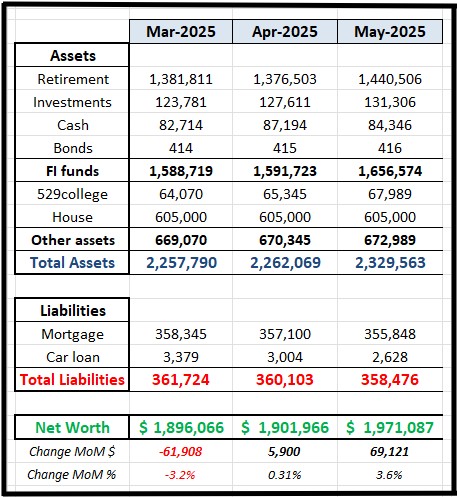

At about $5k, spending in May was a bit higher than usual. But none of the categories stick out.

We’re enjoying summer in our part of the world. Though rainfall has been quite a bit higher than usual. School is over and we’re utilizing the mornings in sports and activities.

We hope you’re enjoying this time of the year, wherever you are. Cheers!

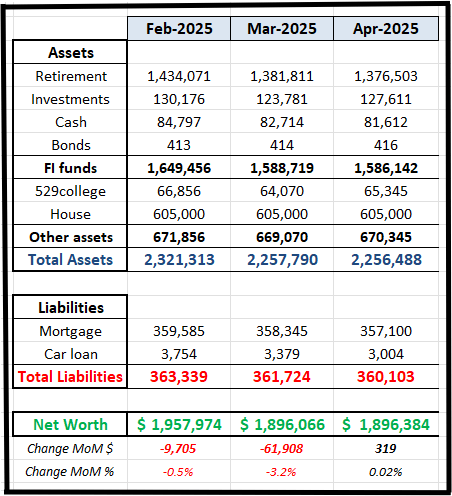

We missed the post in March! Any way, here goes April (with March’s number included).

A bumper loss in March, followed by a wash in April.

Spring sports have been taking over our lives this past two months. Weekends are a blur with plethora of games, all over town, and some out of town. Schools will be done in a couple of weeks and we’ll get some sanity back into our lives. But we love this chaos!

Hope you are enjoying spring as much as we are. Cheers!