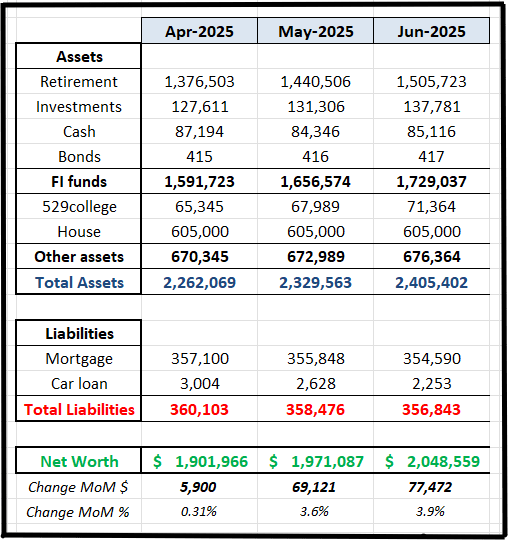

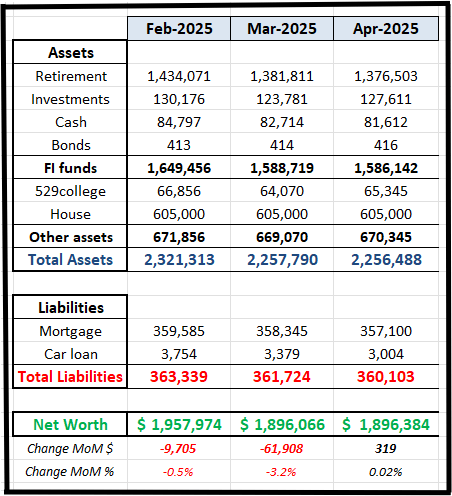

The first update for the year. January and February provided modest increase but in March the bottom sorta fell off. $80k in the red about 3.5% decrease from the previous month.

But it is fine 🙂

Spring sports season is officially underway. Between playing and coaching a combined total of 3 sports, we have little time for much else. We love the seasons where we are outside and active!

Here’s hoping you are having a great start to the year.