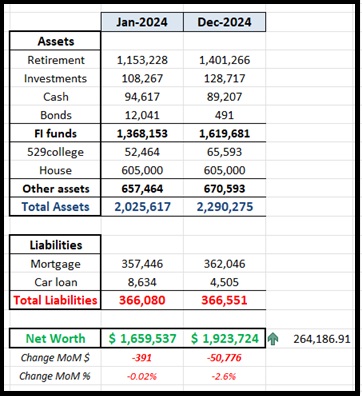

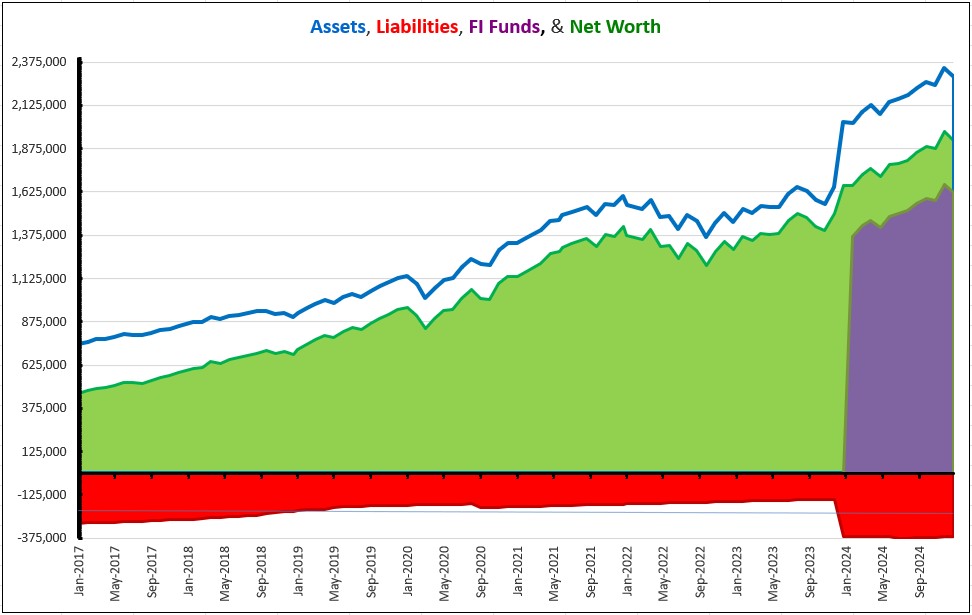

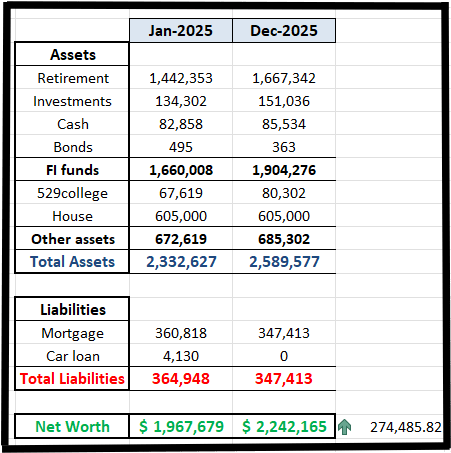

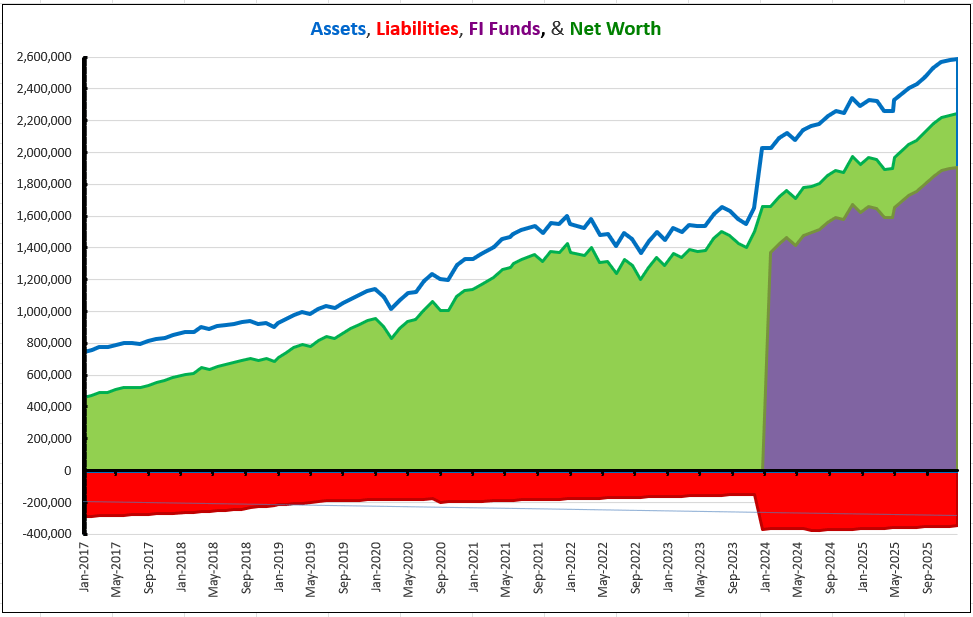

Net worth increased by $274k last year and ended the year at $2.2m.

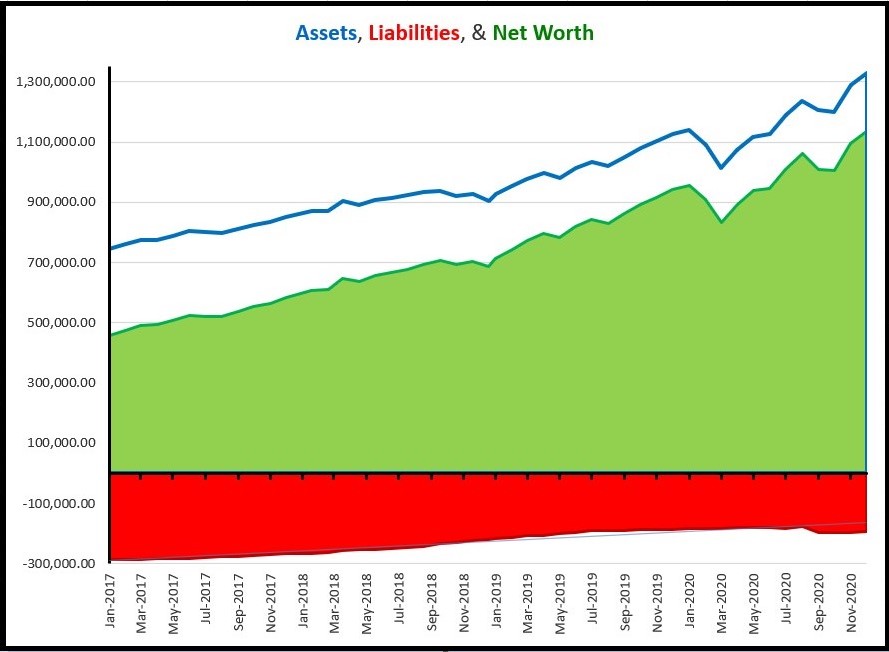

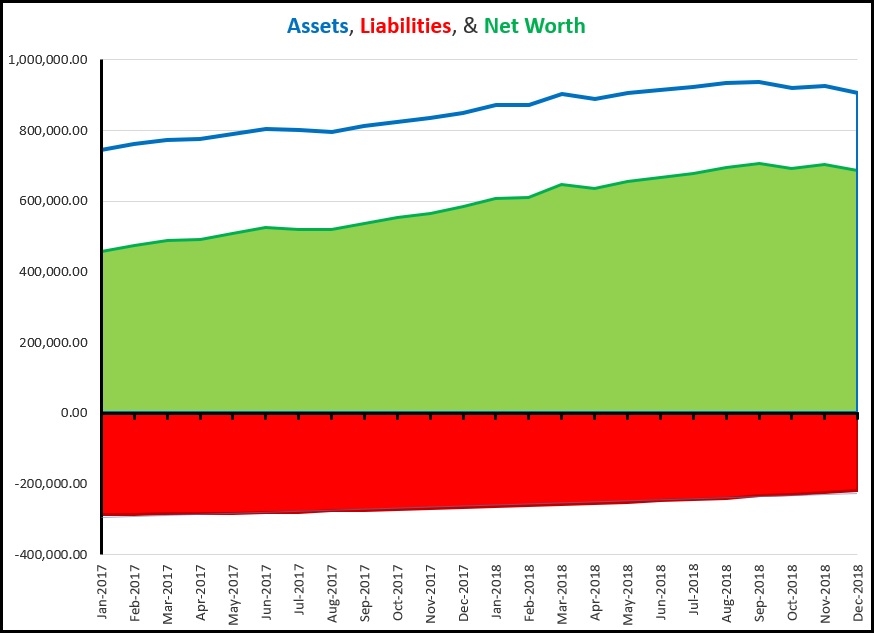

Since we started tracking and documenting our journey towards FIRE from beginning of 2017, we’re amazed how far we’ve come. In January 2017, our net worth stood at $458k. In 9 full years, we are over $2.2m. That is bonkers.

–

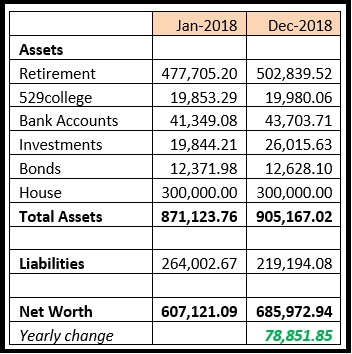

We made the following contributions to our investment accounts last year:

- 401(k) – $17,070 (only for W) – $2,116 more than in 2024 and went over the $15k goal set last year

- IRAs – $14k (combined for both) – hit goal of max limit; as we did in 2024

- Brokerage – $1,900 – was $0 in 2024, and wasn’t a goal for last year

- 529 – $3,400 – $400 more than 2024, and almost hit stretch goal of $3.5k

- HSA – $8,550 – $1,200 paid by employer, so we put in the max $7,350 allowed

In all, we contributed $43,720 to our investments in 2025.

Goal for 2026:

- IRA: Hit max limit of $7.5k individually; $15k for both

- HSA: Hit max limit of $8,750 for families. W’s employer chips in with $1.2k, so out of pocket for us would be $7,550

- 401(k): Hit $17k.

- 529: Minimum of $3.5k. Stretch goal would be $4k.

- ……anything else would be just gravy