This is how much we made in 2025.

- W’s gross income: $165,517

- M’s gross income: $39,789

Our total yearly gross income is $204,306

This is more than $14.8k than we made in 2024.

This puts us in the top 15% of US household income.

A no-holds-barred approach to personal finance where we bare all our gory details, ahem, numbers. Anonymously.

This is how much we made in 2025.

Our total yearly gross income is $204,306

This is more than $14.8k than we made in 2024.

This puts us in the top 15% of US household income.

Earlier this month, Vanguard published this report on FIRE and set some anti-FIRE cats amongst the proverbial pigeons. You know, pigeons like us who have bought into the “idealogy” that you really can’t afford to be chained to a job for a paycheck for decades and decades. You need to get out of the rat race as soon as you can, as if your life depended on it.

The article, bullet-wise (as all good articles should have), talks about:

All true. And most rational people pursuing/in FIRE would say so. These factors are nothing new. The 4% SWR is not gospel, the recent returns of stocks is the outlier than the norm, investing costs are to be merciless slashes, diversifying, and having a spending strategy – and even an earning strategy in FIRE – that is flexible, are all built into the plan!

Here is the real, inflation adjusted, historical return YoY (CAGR) of the stock market since 1871. Yes, over 150 years worth of data. It stands at 7.06%, adjusting for inflation and reinvesting dividends, for over a century and half. You can select the time period you want – MoneyChimp Market CAGR.

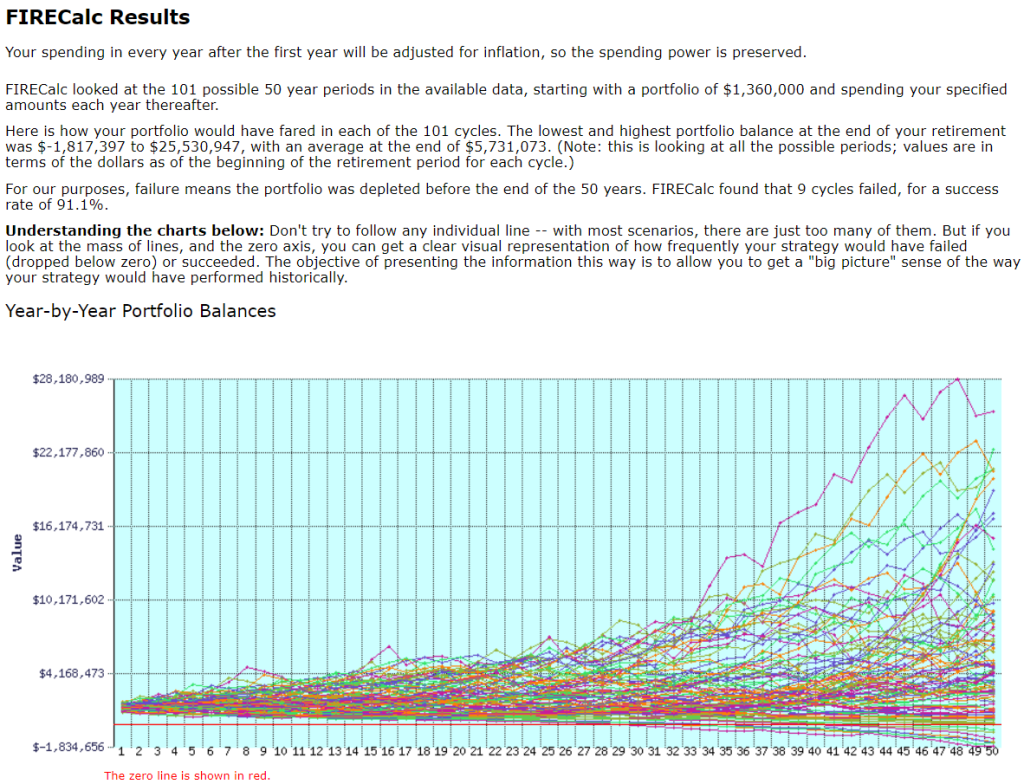

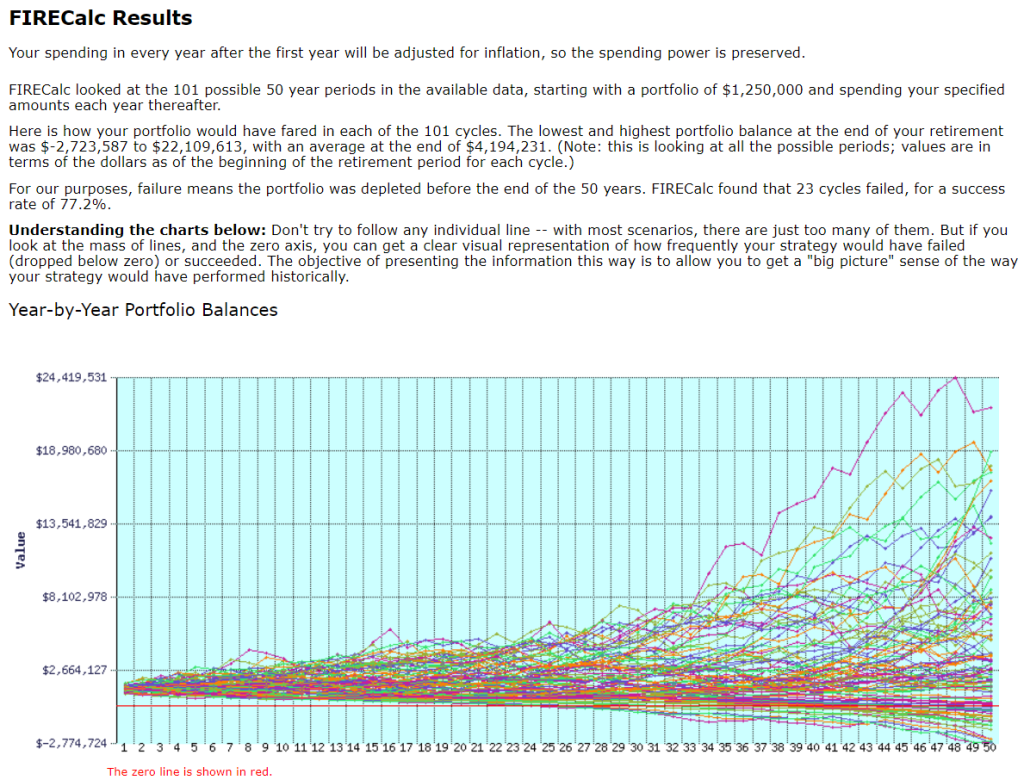

Here are two simulator applications, that runs multiple iterations (hundreds) of how a portfolio performs over extended draw down periods. I’ve run 3 simulations on each. (there are some underlying assumptions, such as stock/bonds allocation, expected inflation, etc. I encourage you to explore and play with the tools):

Scenario 1 – Success rate of 99%

Scenario 2 – Success rate of 93%

Scenario 3 – Success rate of 84%

firecalc (running the same 3 scenarios)

Scenario 1 – Success rate of 96%

Scenario 2 – Success rate of 91%

Scenario 3 – Success rate of 77%

If someone told me that I’d have between 77% and 84% success rate of an endeavor that I was about to embark on, I’d take those risks. But we are almost hard wired to be extra cautious about money. Especially our own money. So I understand if the 4% rule is bent into the 3.33% rule to get into the the 90% certainty range.

And, Vanguard keep those costs low. We’re all good here.

Yes, carriers – plural.

We had been with T-Mobile for about 12 years. Our monthly bill, for a family plan of two, had averaged out to around $75/month for the past couple of years. Not bad. We were grandfathered into an old plan and didn’t quite think much about it.

But starting this year, T-Mobile dropped the corporate discount we used to get. Monthly bill jumped to $84. Just a $9 increase, still it got me thinking if other comparable options were out there with a lower cost.

After a bit of research and a lot of procrastinating, we finally pulled the trigger to switch in August.

W went with Google FI. You pay $20 for unlimited calls and texts, and $10/GB of data used. One month cost was $32. This is post paid with users only paying for the amount of data they use. Coverage is quite possibly even superior to Verizon as Google FI uses combination of any available network and wi-fi spots. Can keep old number.

M went with Mint Mobile. This is a prepaid MVNO operating on the T-Mobile network. They have “free” unlimited talk and text on all of their plans. You “only” pay for data. Paid upfront $66 for 6 month, with 8 GB of 4G LTE data every month. That works out to $11 a month. This is a promotional offer that anyone can avail. Regular priced plans start at $15/month for 12 months, for 3 GB of data every month; and other combinations of number of months and data limits – all prepaid. Coverage is same as T-Mobile. Can keep old number.

By switching we have effectively cut our phone bill in half, with same or better coverage. Boom.

The basic premise of this post is this:

You should get the longest term mortgage that you can get. Say, 30 years.

You should try to pay it off much faster. Say, 10 to 12 years.

Note: If on the 30-year mortgage you were to pay every month as if you were paying a 15-year mortgage, you WILL NOT be able to pay off your 30-year mortgage in 15-years.

It will take you a few more payments, depending on the rates of each mortgage. That is the premium you would be paying for having lower monthly payments, but with a greater rate of interest.

But, let’s suppose, you were to pay your 30-year mortgage as if it were a 10-year mortgage, you WILL pay it faster than if you took out a 15-year mortgage and paid the standard calculated mortgage payment every month.

As an example, let’s work with the following numbers. Here is the link to the Google sheet that lays out the numbers …in all their gory details 😀

(Rates are from about 5 months ago)

Principal mortgage amount: $300,000

Rate on a 30-year mortgage: 4.5%

Rate on a 15-year mortgage: 3.875%

If you were to take out the 30-year mortgage, and if you were to make the full 360 payments, you will end up paying $247,220 in interest on your $300k loan.

But we don’t want to do that. This is the control option. We want to know what the interest number is but we will not be following this option.

If you were to take out the 15-year mortgage, and if you were to make the full 180 payments, you will end up paying $96,057 in interest on your $300k loan.

Now …the scenario we want to focus on.

In this scenario, you are paying your 30-year mortgage as if you were paying down your 15-year mortgage – i.e. you are rounding off your monthly payment to what would amount to if you were paying a 15-year mortgage, an extra $680.26 that goes directly in reducing your outstanding principal every month. In this case, you end up paying $120,893 in interest, and you pay this over 192 payment.

More than a 50% decrease from $247K to $120K. Voila! But still more than what you would pay for a 15-year ….

Why 192 payments? Because it won’t be 180 payments as less is going towards paying down the principal than if you actually had a 15-year mortgage. This amounts to paying around $96 more in per month for what I call the “premium for safety” that you pay for not taking out a 15-year mortgage.

Whew. Still with me? We have one more scenario to cover.

Now …we come to the scenario that I really want to focus on.

Look into the second sheet/tab in the worksheet.

What if you were to pay down your 30-year mortgage as if you’re paying a 10-year loan (with the rates from the 15-year loan).

You would end up paying only $76,035 in interest and pay off your mortgage in 125 months (still more than 120 payments if you actually took out a 10-year mortgage, but close enough).

I’ll repeat the theme of this post here again: Get a 30-year mortgage. Then pay it down as if you were paying a 10- or 12-year mortgage.

You will pay far less in interest, $20K in our example. But you also have the option with a lower monthly payment if you cannot accelerate fast enough.

There you go. Download the worksheet and play around with your own numbers.

_____________________________________________________________

There is one more scenario which in the third sheet, that tells you what is the optimal number of payments you should aim for if you want to come closest to paying the total interest if you had a 15-year mortgage. In this case it comes out to 148 payments.

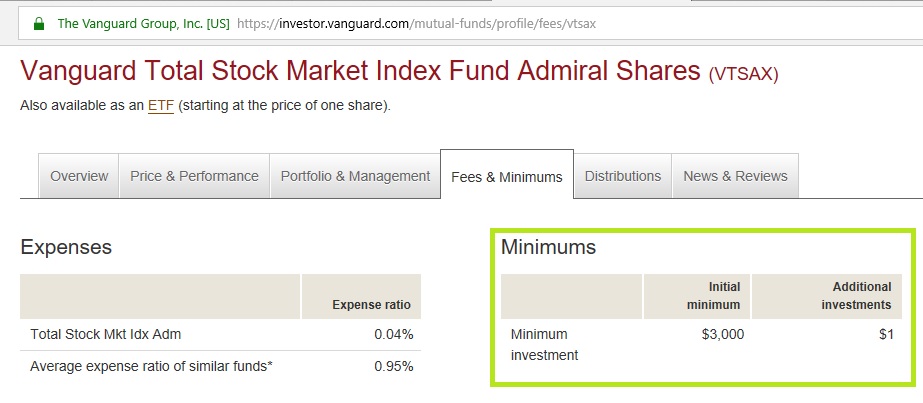

On Monday, November 19, Vanguard announced that they are lowering the minimum investment for Admiral shares on 38 index funds, VTSAX being one among them. The earlier minimum was $10k so this is a big deal for regular investors.

You read about the announcement here.

Even less reason for anyone to invest!

As to why you SHOULD be investing in VTSAX, because the “Godfather” says so!

The IRS came out with a directive on Nov 1, 2018 announcing changes to contribution limits in 2019.

Here’s in a nutshell what is changing.

You can read the original directive here or the technical guidance here.

Cheers to more saving!

Say it to the tune of “Are we there yet?” your kids invariably sing when you’re taking them on a road trip 😅

Our blog was recently added to the Rockstar Finance directory of all personal finance blogs. I had no idea about this aggregator site before a fellow newbie blogger mentioned it.

You can find us at the recently added list or the main list. We clocked in at #149.

Though this means that we’re officially a part of the FIRE blogosphere, we are far, far away from being the rock stars of the demography that preach sensible personal finance. There are giants in this field and we learn and incorporate the portions that applies to us, in this phase of our lives.

Which bring me to the next point. And it is a rant. For which I’m apologizing right now. Having mentioned earlier that this is a judgement free zone, the next portion is going to sound hypocritical. But the incredulity of the stated facts are just too …well, incredible, for me to not lose my mind.

While going through some of the blogs there were recently added to the Rockstar Finance directory, I came across this blog maintained by a lawyer. I will purposely not name this blog nor reveal the gender of the writer. This is not meant to vilify the person behind the blog, nor give them added eyeballs. This is meant to show how stretchable our various aims and goals are.

This person claims that they need access to a gym that charge $893. Monthly.

MONTHLY $893 gym expense. A completely discretionary expense. Let that sink in.

Despite the fact there is a student loan that is more than the average sized mortgage. Despite living in a city with high costs. Despite having a $30k car loan at 3.5%. All the above factors are perfectly fine, even when taken in aggregation. But all these debts, plus a $893 monthly spending habit is another thing. Not only does this individual have zero qualms about it, the blogger goes on to make an astounding appeal to the readers to not cancel their own expensive gym membership. This is where it got my goat.

I am dumbstruck. I mean I’m sorry that I’m even doing this, but this affects me viscerally.