In the first post of this blog we mention that our goal is to be financially independent by 50. What this means is that at this point in our lives all our expenses will be funded by our investments, and we will have no need for any active income coming in.

But HOW? To answer that first we have to take a couple of steps back. If you have read about the 4% withdrawal rate (and if you haven’t, please read that first; right now! and all the other posts under the Stock Series by Mr. Collins) you know that once you’ve saved enough where you can comfortably withdraw from your nest egg at the rate of 4% each year, you are set. Also, check this out by MMM. And this in-depth post by the MF.

The question then becomes, what is the amount you need saved. Let’s call this x.

What drives this x? Your expenses! When you’re FIRE you’re not saving, per se, anymore. You’re only looking to get the necessary amount every month for your expenses. We will talk about post-FIRE expenses more in a detailed post later. Let’s call our post-FIRE annual expenses y.

So, y = 0.04x

Pretty simple, huh?

Therefore, x = y/0.04 => x = 25y. Our total savings need to be 25 times our annual expenses. That it’s.

If only we could determine y, our spending, we will know how much we need to save up, x.

We have determined that our spending when we are FIRE will be $48,000 per year, at the most. Again, we’ll publish a post detailing this. For now, just know that this $48k does not contain any mortgage payment or college tuition for our child.

Plugging in, our “Retirement” bucket need to be $1,200,000 before we are FIRE.

The last step now. How long do we need to save till we have $1.2M in our retirement accounts?

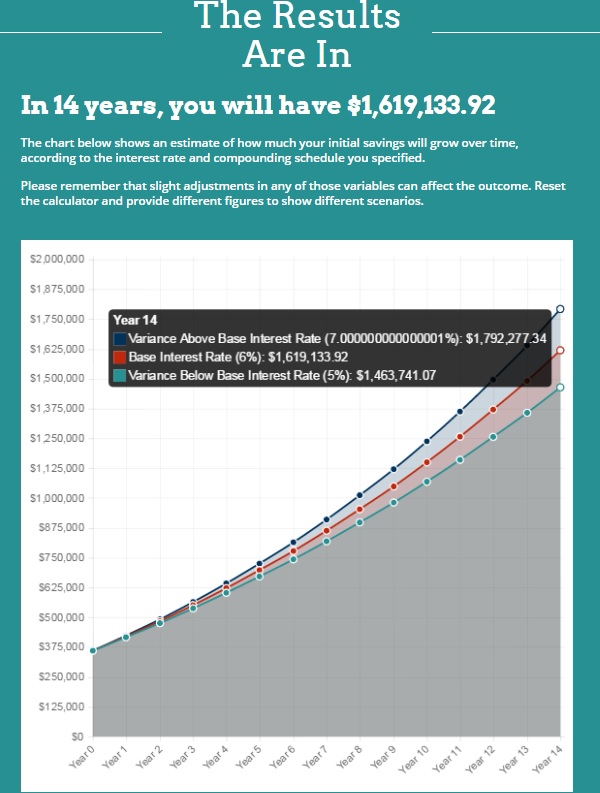

In January of 2017 we had $359,774.81 in our retirement accounts. Currently we are pumping in $3,195 every month into retirement accounts. Assuming a return of 6% annually, in 14 years, using this calculator we will have accumulated $1.6M. That is over $400k more than we need!

Few assumptions here:

– An annualized return of 6% over a long time period is very conservative in the first place. Also, as you’ll see in the screenshot, the tool gives your projection if your annualized rate was 5% and 7%. Even with a 5% return we still beat our projection of $1.2M!

– Assumed interest compounded annually, which is again the most conservative estimate

– We have assumed the monthly pay-in of $3,195 as a constant over these 14 years, when in practice this will certainly increase every year.

– We are basing our projections ONLY on the retirement accounts whereas we’ll actually have money in our regular bank accounts and other investments.

In short, all of our assumptions are on the VERY conservative side. Quite possibly we should be able to retire even earlier than the 50-year old mark that we have set for ourselves.

This FIRECalc tool is a great way to see the probabilities of how your money will last in retirement.