The other day I met an affable Financial Planner who’s looking to go to the same grad school as I had been to. We were talking and at some point the topic of fees arose in our discussion. This FP wasn’t pushy or trying to oversell the value of planning for the future but was still a bit coy about really admitting how fees add up. And rightly so, because her livelihood depends on the fees! This is the operating model of any FP, they make money off the fees they charge to maintain your money. I have nothing against her but this got me thinking how fees add up, even little marginal ones such as 0.061%.

Let me illustrate this point by taking a look at my 401(k) investments and then compare it with the what-if scenario of putting the exact same amount in Vanguard index funds. I have to start off by acknowledging that I’m lucky to have a 401(k) plan that has low fees. Lower than a lot of other places. This article says that the average expense ratios for equity mutual funds in 401(k) plans is 0.48%.

Before I started to look around I didn’t really think the average would be so low. Nonetheless we’ll run with this. In the table below you’ll see the actual breakdown of my investments in my company’s 401(k) plan.

I have money in a bond fund, a targeted date fund, a large cap fund, a mid/small cap fund, an international fund, and in my company’s stock. All funds are Vanguard institutional funds and the operating expense ratios of all the funds are very low. Kudos to my employer!

Side note: We can debate the efficacy of using 5 different funds to hold the money, but let’s keep that for another day!

What skews the perfectly low ERs are the Administrative Expense of 0.08% that our 401(k) administrator, in this case Aon Hewitt, systematically charges across the board.

My weighted average ER comes out to 0.111%. Not bad at all for being 4 times lower than the average! But still higher if not for the dang administrative expenses.

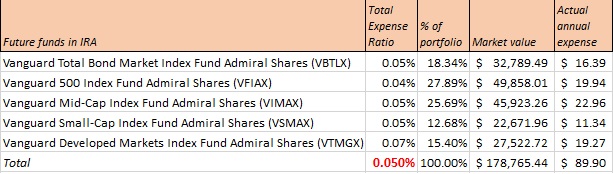

Now let’s assume that I take this money out today and roll-over into an IRA, and invest in similar Vanguard funds.

I have made a couple of adjustments, while keeping the weights of the bond, large cap, and international funds the same.

- Kept the same weight for the mid/small cap from the 401(k) and rolled into the VIMAX Midcap fund in the IRA.

- Rolled the ESOP and target date fund from the 401(k) into VSMAX Small cap fund in the IRA

With these changes, my new weighted average ER comes down to 0.05%. Compared to the 401(k), that’s a difference of 0.061%.

Again: We can debate the detriments of not just using VBTLX and VTSAX, another day ….

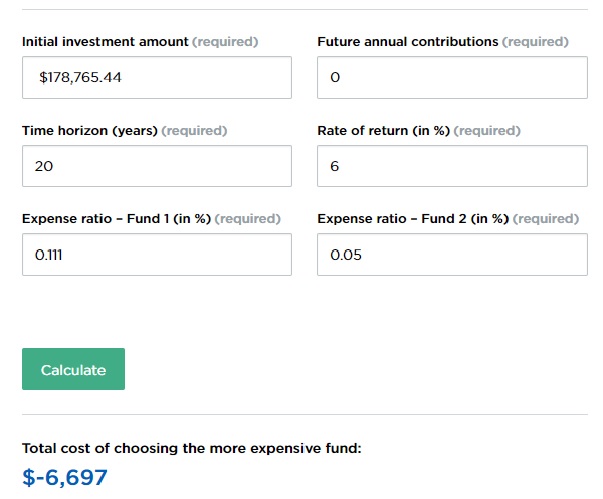

This change would result in almost $7k in extra money over a period of 20 years, at 6% annualized return. Plug in your numbers here. I’ve deliberately left the future contribution cell blank to have apples to apples comparison.

Dear readers, would love to know how your 401(k) plan expenses compare.

Good for you, 6FF, for taking the reigns of your finances in your hand! A fee of 1.97% is insane 😀

Now to go and check out your blog.

LikeLike

We just moved our IRAs from an advisor to Vanguard. Counting ER and the AUM fee we were paying 1.97%!!!!!! Our weighted average ER was 0.62%. I haven't calculated the new weighted ER with vanguard, but I'll be saving myself thousands this year alone and who knows how much in future return. I'm a huge advocate for index funds now.

LikeLike

Yes! This Financial Planner was indicating that her fees are around the 1% mark and I was figuratively rolling my eyes while listening.

LikeLike

I always find it incredible how small changes in fees really add up over time. You are paying thousands of dollars extra over time for just a 0.061% difference. Imagine how much extra a 1% difference makes. Ouch.

LikeLike